The SigTech Risk Premia Report provides comprehensive performance analysis of diverse risk premia strategies across commodities, equities, fixed income and FX asset classes. They are structured in a long/short setting to minimize directional effects from the underlying asset class.

Our strategies emphasize transparency, a sound underlying economic rationale, tradability and a consistent methodology across strategies. Recent enhancements to the SigTech’s monthly Risk Premia Report include:

- Composite strategies: Analytics for five risk premia composite strategies and a multi risk premia strategy allocating across all 19 strategies.

- Extended analytics: In-depth risk analytics and extended returns data for a granular strategy assessment.

- Improved methodology: Revised underlying methodologies for the risk premia strategies, including extended investment universes and definition of risk factors.

- New risk premia category: Though tail risk is not a traditional risk premia strategy, it has been added for its strong diversification properties.

What are risk premia strategies?

A risk premia investment strategy isolates and systematically harvests excess returns from exposure to a specific risk factor such as value, momentum or carry. Such strategies are used by hedge funds, asset managers and asset owners as building blocks when creating systematic investment strategies and diversified portfolios.

Brief history

The academic foundations of risk premia were laid in the 1950s when Markowitz published his seminal work around Modern Portfolio Theory. His groundbreaking research showed that the return of an asset is a function of its underlying level of risk. Drawing on this observation, Sharpe later introduced the Capital Asset Pricing Model (CAPM), which defines a single market factor (market beta) as explaining an asset’s return.

r = rf + β(rm-rf)

As the influence of these approaches grew, it became apparent that additional variables were needed to more comprehensively explain returns. As an extension to CAPM, Fama and French introduced their highly acclaimed 3-factor model, adding size and value as explanatory variables. This was later expanded upon by Carhart who added the momentum factor to what has become known as the 4-factor model,

r = rf + β1(MKT) + β2(SMB) + β3(HML) + β4(WML)

where MKT is the market factor, SMB is the size factor, HML the value factor, and WML the momentum factor.

In recent years, the number of explanatory variables – or risk factors – has exploded. Famously, Harvey and Liu minted the expression “factor zoo” when arguing that factor production had become “out of control”. The authors have identified more than 400 factors presented in academic papers which are claimed to generate positive risk premia.

The existence of classic risk premia such as value, momentum and carry is mostly undisputed. This can be contrasted with more esoteric factors (i.e. lottery demand, hiring rate, and non-myopic beta) which lack wide-spread recognition. In addition, it is important to note that many of the newer factors have a strong commercial link, which raises concerns about their academic objectivity. To find out more, you can access Harvey’s “factor zoo” list here.

Key risk factors

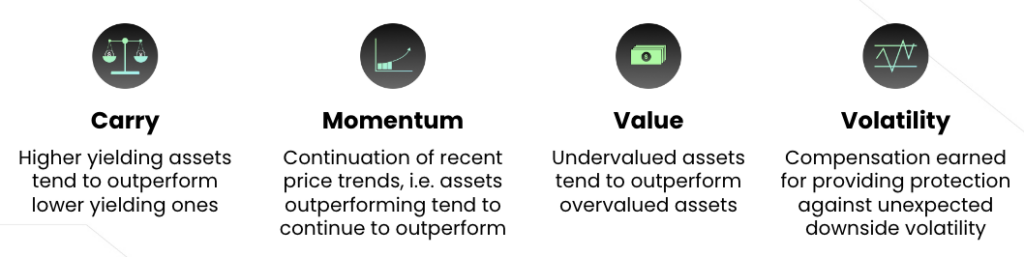

The existence of risk factors and their corresponding premia is explained by various structural conditions or behavioral biases and can be supported by sound economic rationale. For example, the tendency for asset prices to revert to a long-term fair value (mean reversion) underpins the value factor, herd mentality can explain momentum, and mispricings due to supply/demand imbalances can result in carry opportunities. Furthermore, the strong growth of the derivatives market has resulted in larger and more frequent supply/demand imbalances which create opportunities in the volatility space.

SigTech’s risk premia

Using our market leading quant analytics and backtesting platform, we have built a set of risk premia strategies presented in our monthly benchmark report. The report provides a comprehensive risk/return overview alongside commentary on cross-asset risk premia.

As the number of risk factors used to create risk premia strategies has expanded exponentially, it is important to define the underlying fundamental principles that the strategies should comply with.

The four fundamental requirements of risk premia

Risk premia are either structured as long/short (“alternative risk premia”) or as long-only portfolios (“smart beta”). SigTech’s risk premia strategies are long/short portfolios and cover the asset classes (i) equity indices, (ii) equity single stocks, (iii) fixed income, (iv) FX, and (v) commodities. We calculate risk premia for each asset class using the following risk factors:

The fundamental principles mentioned above serve as a guideline for SigTech’s risk premia strategies. In addition to applying a fully transparent methodology, we place great emphasis on a sound underlying economic rationale, tradability, and – perhaps most importantly – applying as consistent a methodology as possible across our various strategies.

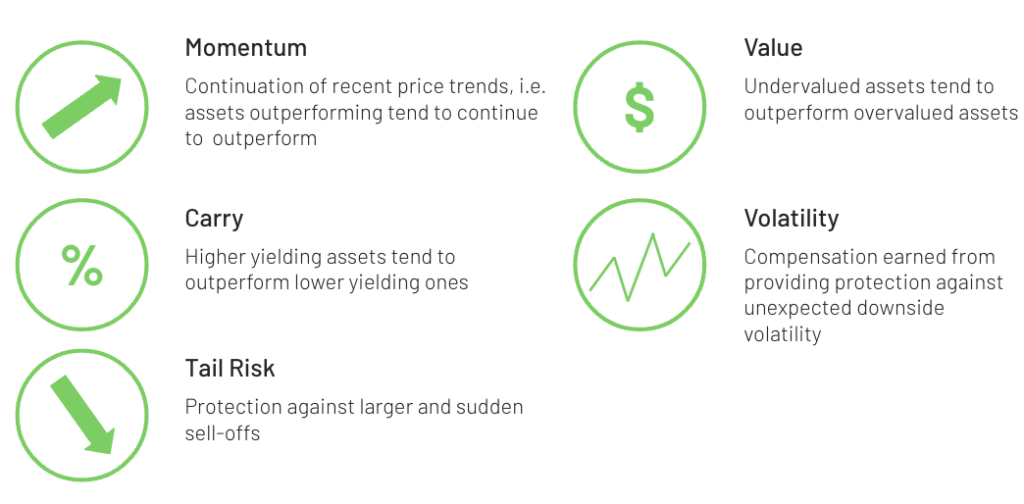

The strategies cover the liquid asset classes: commodities, fixed income, FX and equities – distinguishing between equity index and equity single stock strategies. We focus on the most common risk premia; value, momentum, carry and volatility, as well as a recently added tail risk strategy. Whilst tail risk is not a traditional risk premia strategy, we chose to include it due to its historically attractive diversification properties during larger sell-offs and the increasing popularity of systematic tail risk strategies among institutional investors. Please see our Alternative Risk Premia whitepaper to get detailed strategy descriptions.

Creating bespoke risk premia

SigTech’s quant technology platform offers investors access to a sophisticated quant analytics and backtesting platform with clean and curated data across asset classes. Applying SigTech’s transparent and modular framework enables you to efficiently create bespoke risk premia strategies based on your individual requirements and situation.

In addition to changing the underlying methodology, the granularity at which you can customize your strategies is almost limitless. For instance, you can impose limits on concentration risk and leverage, apply FX (foreign exchange) hedging, take specific trading commission rates into account, your market impact assumptions, current market conditions, and factor in specific tax situations.

Risk premia strategies have a long and varied history in investing, but remain valid to this day. By adding bespoke risk premia in their investment portfolio construction to achieve attractive risk-adjusted returns, investors see a myriad of benefits.

- Improved diversification: complementing traditional asset class diversification, they enhance the expected risk/return profile by diversifying across risk factors

- Reduced costs: cheaper implementation and running costs compared with (often externally managed) alternative investment strategies with similar risk/return profiles

- Improved transparency: in-house implementation provides fully transparent investment methodology and a complete look-through at security level

- Efficient tactical trading: efficient implementation of tactical investment convictions by tilting the portfolio to specific risk factors

- Speed and scale: improve flexibility and accelerate the research process when creating bespoke investment strategies

- Improved liquidity: underlying investments in highly liquid securities facilitates immediate trade execution with limited slippage

- Benchmarking: can be used to benchmark investments in other types of alternative investment strategy

Interested in creating your own multi asset risk premia strategies?

Risk Premia Strategies – FAQs

What is a risk premia strategy?

Risk premia strategies aim to systematically isolate and harvest an excess return stemming from exposure to specific risk factors, including carry, momentum, value and volatility.

Why add risk premia strategies to a portfolio?

The main reasons investors allocate to risk premia strategies are to:

- Improve portfolio returns

- Increase diversification and reduce overall portfolio risk

Which are the best performing risk premia strategies?

Risk premia strategies gain systematic exposure to specific risk factors and are thus dependent on the performance of those factors. The performance of risk factors is cyclical and no single risk factor exhibits a superior performance in all market environments.

To smooth the return of individual risk premia strategies, multi factor/asset strategies allocating to multiple risk factors are created.

To follow the performance of various risk premia strategies, subscribe to SigTech’s monthly risk premia report.

How do investors use risk premia strategies?

Depending on the investment objective, investors can allocate to risk premia strategies with a long-term buy-and-hold perspective or implement shorter-term tactical tilts (e.g. profiting from undervalued stocks outperforming overvalued stocks).

For what asset classes can you create risk premia strategies?

One of the key characteristics of risk premia strategies is tradability, i.e. they are resilient to transaction costs and liquidity constraints. Risk premia strategies are thus suited to liquid asset classes such as equities, fixed income, FX and commodities.

How can SigTech help me build risk premia strategies?

As part of its 100+ available investment strategy templates and functionalities, SigTech’s quant technologies platform offers users access to a wide range of ready-made – but fully customizable – risk premia strategies.

Disclaimer

This document is not, and should not be construed as financial advice or an invitation to purchase financial products. It is provided for information purposes only and is subject to the terms and conditions of our disclaimer which can be accessed at: https://www.sigtech.com/legal/general-disclaimer